Brand Valuation: Why 92% of Corporate Value Is Now Invisible

A brand can be worth eight figures and still show up as a zero in the accounts.

That’s not a quirk of bad bookkeeping – it’s how UK and international accounting standards are built.

Intangible assets built in-house don’t get capitalised, no matter how much revenue they protect or how much premium they command. Only brands that have changed hands through a transaction receive a number.

For a CEO or MD running a 50–200 person UK professional services firm heading toward a growth phase, an acquisition, or a repositioning, this gap is not academic.

Ocean Tomo’s Intangible Asset Market Value study puts intangible assets at roughly 92% of S&P 500 market capitalisation by the end of 2025, up from 17% in 1975 and 68% in 1995. Most of that value sits entirely outside the accounts.

Request a free brand audit, and you’ll usually find the same pattern: firms that have never quantified their brand equity are the ones most likely to under-negotiate it the day someone else tries to buy, merge with, or invest in the business.

- Intangible assets now make up about 92% of S&P 500 market value, yet most brand value remains invisible in statutory accounts.

- Brand valuation assigns a monetary figure via cost, market, or income methods; only acquired brands are capitalised under IFRS 3 and UK GAAP.

- Measure and track your in-house brand KPIs quarterly; adopt a two-asset model so you can defend value before a buyer's due diligence prices it.

What Is Brand Valuation?

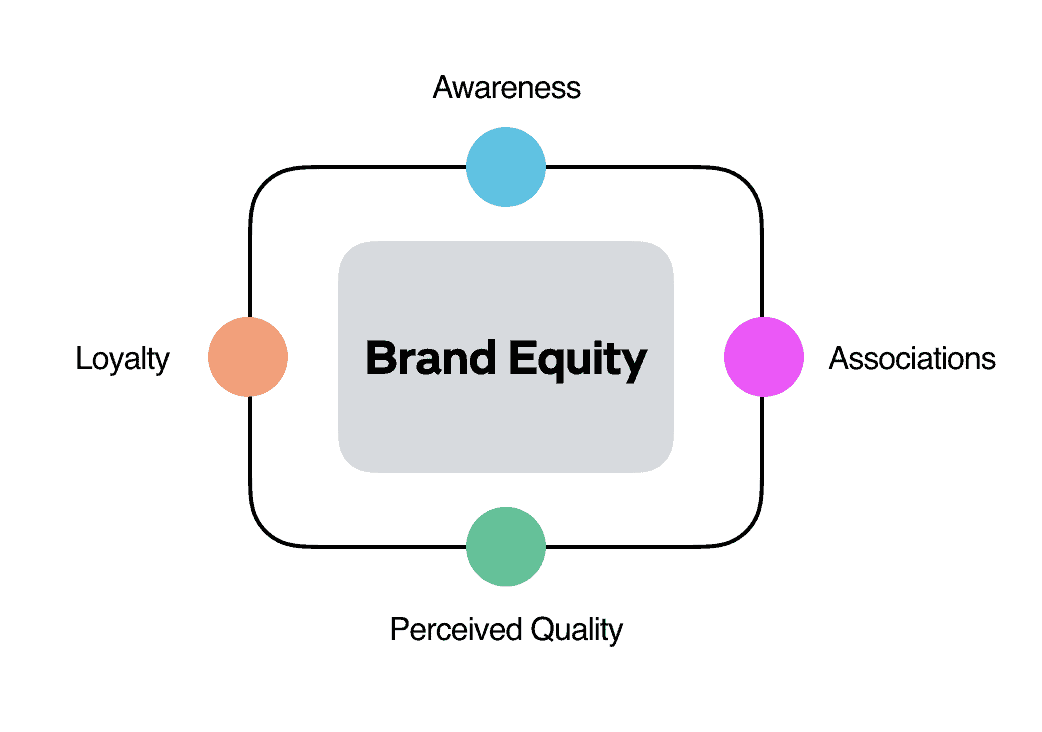

Brand valuation is the process of assigning a specific monetary figure to a brand using one of three recognised methods: cost-based, market-based, or income-based. It differs from brand equity, which describes the strategic and psychological value a brand holds in customers’ minds without attaching a number to it. Valuation turns that perception into a figure a board, an acquirer, or an auditor can act on.

- Brand valuation produces a currency figure; brand equity describes strategic and perceptual strength without one.

- Three methodologies exist – cost-based, market-based, and income-based – each suited to a different commercial scenario.

- Accounting standards permit a brand’s value to be recognised on the balance sheet only after an arm’s-length transaction.

Brand valuation assigns a specific monetary figure to a brand using cost, market, or income-based methods. Still, accounting rules allow that figure on the balance sheet only after the brand has changed hands in a transaction.

Why This Matters for a Firm Preparing to Rebrand, Merge, or Sell

Kraft Heinz Company gives the clearest public demonstration of what happens when brand value is mismanaged rather than measured.

In February 2019, Kraft Heinz Company disclosed a $15.4 billion goodwill impairment charge, of which $8.3 billion was directly attributed to a loss in value of the firm’s Kraft and Oscar Mayer brand intangibles.

The disclosure triggered a 27% single-day share price fall, and Harvard Business School’s case study on the write-down – authored by Professor Jill Avery – frames it as a direct consequence of cost-cutting decisions that eroded brand equity faster than management tracked it.

That’s a listed multinational, not a 90-partner accountancy firm in Leeds. But the mechanism is identical at any scale: a brand that is not actively measured cannot be actively defended, and the first time many boards discover their brand’s real financial exposure is during due diligence, when the buyer’s advisers do the measuring instead.

Every acquirer prices your brand, whether you’ve priced it yourself or not. The only question is who’s holding the better evidence in the room.

The Anatomy: Three Ways to Put a Number on a Brand

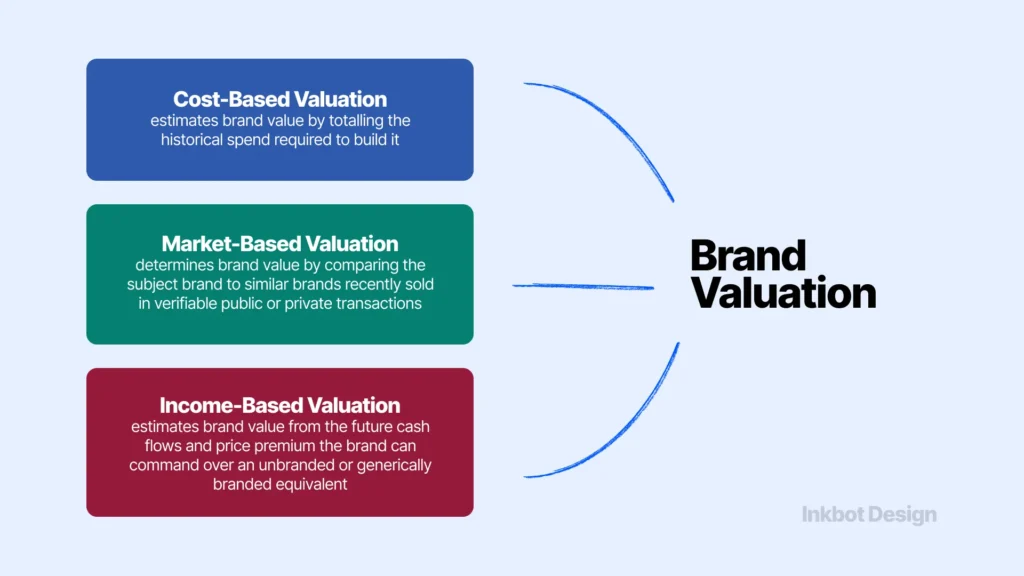

Cost-Based Valuation

Cost-based valuation estimates brand value by totalling the historical spend required to build it – design, trademark registration, marketing, and positioning work – rather than by measuring what the market would pay for it today.

This method is common in early-stage acquisitions, where a target has spent heavily on brand-building but has no trading history long enough to support an income projection.

It answers “what did this cost to build,” not “what is this worth now” – a distinction that matters because the two figures rarely match.

A firm that spent £40,000 on a rebrand five years ago and has since become the recognised name in its regional sector has a cost-based valuation that badly understates its actual commercial worth.

Cost-based valuation is the floor, not the ceiling. Use it to establish a defensible minimum, never a target figure.

Market-Based Valuation

Market-based valuation determines brand value by comparing the subject brand to similar brands recently sold in verifiable public or private transactions, using those deal multiples as a benchmark.

This is the method used for what HBS Online’s guide to brand valuation calls “home-grown” brands without their own acquisition history – the valuer instead borrows evidence from comparable deals elsewhere in the sector.

The limitation is obvious in professional services: genuinely comparable transactions are rare, deal terms are frequently confidential, and a law firm merger in Manchester tells you very little about what a specialist tax advisory brand in Edinburgh is worth.

Market-based valuation works well in sectors with high transaction volume and public disclosure – technology, consumer goods, financial services at scale – and poorly in sectors where deals are private and infrequent.

Income-Based Valuation

Income-based valuation estimates brand value from the future cash flows and price premium the brand can command over an unbranded or generically branded equivalent, typically using a relief-from-royalty or excess-earnings model.

This is the method preferred by firms with an established trading history and is used by companies like Lego, according to HBS Online’s brand valuation guide.

For a professional services firm, the practical version of this question is blunt: could you charge the same fee, retain the same clients, and win the same pitches under a generic, unbranded name?

The gap between that hypothetical fee and your actual fee – capitalised over time – is your income-based brand value. It is the most defensible method for an ongoing business, and the one most acquirers will reach for during due diligence.

Where People Get It Wrong

The most common mistake is not choosing the wrong valuation method – it’s assuming that having a valuation figure means having a balance sheet asset. It doesn’t.

Purchased goodwill and purchased trademarks are capitalised because IFRS 3 and equivalent UK standards require a transaction to establish objective, verifiable value.

In-house brand equity – the value a firm builds organically through client relationships, market reputation, and consistent positioning – is deliberately excluded from capitalisation, precisely because there is no transaction to verify it against.

That’s accounting conservatism working as intended, not a failure of the system.

The second mistake compounds the first: treating that accounting exclusion as proof the brand has no financial reality. It has plenty.

It simply lives outside the numbers that show up in statutory accounts, which is exactly why a structured brand valuation exercise – conducted before a transaction forces the question – puts a firm in a stronger negotiating position than waiting for a buyer’s due diligence team to do the measuring unilaterally.

Worked Example: A Rebrand Before Exit

Consider a 120-person UK management consultancy, three years from a planned partner-led exit, going through a repositioning ahead of a planned sale.

Under the cost-based method, the firm’s brand carries perhaps £180,000 of accumulated design, trademark, and campaign spend – a figure that would barely register in a deal valued at eight or nine figures.

Run the income-based method instead. The firm charges a premium day rate compared to unbranded local competitors, has a client retention rate materially above the sector norm, and wins a measurable share of pitches on reputation rather than price.

Capitalise that premium over a reasonable multiple and the brand’s income-based value runs into seven figures – a number close to what a private equity buyer’s advisers would independently derive during due diligence, and one the firm can now defend with its own evidence rather than accepting the buyer’s first offer.

That’s the commercial function of a valuation exercise before an exit: it converts an assumption (“our brand is strong”) into a defensible number that the seller’s own advisers put on the table first.

The Sharper Way to Think About This: Brand Equity as Two Assets, Not One

Most explainers on brand valuation present it as a single exercise – pick a method, produce a figure, done. That’s an oversimplification once you sit inside the accounting reality.

Intelligent finance directors resist treating brand value as a single line item for good reason: mixing a verified, transaction-tested figure with an unverified internal estimate would violate the conservatism principle that keeps financial statements trustworthy.

That caution is correct. The mistake is stopping there instead of building a second, parallel structure for the part that accounting rightly won’t touch.

The more useful model treats brand equity as two distinct assets, managed differently:

Asset A – Recognisable, transaction-tested intangible.

This is acquisition goodwill or a purchased trademark: capitalised on the balance sheet under IFRS 3 or UK GAAP because a real transaction established its value.

It’s audited, amortised or impairment-tested, and behaves like any other financial asset – including the downside risk Kraft Heinz Company demonstrated in 2019.

Asset B – Separately managed, non-capitalised strategic intangible.

This is in-house brand equity: never capitalised, but tracked through mandatory narrative disclosure in the annual report or investor materials, and linked to a defined KPI schedule: client retention rate, price premium versus the sector benchmark, pitch win rate attributable to brand recognition, and unprompted brand awareness within the target market.

Firms that adopt this hybrid model don’t try to force Asset B onto the balance sheet.

Instead, they maintain the KPI schedule as a living document, updated quarterly, so that when a transaction, funding round, or partner buy-in eventually creates the trigger event for Asset A treatment, the firm walks into that negotiation with two to three years of evidence rather than a single valuation report commissioned the week due diligence started.

The Verdict: Measure the Asset Before Someone Else Prices It For You

Brand valuation is not a marketing exercise dressed up in financial language.

It’s the mechanism by which a real commercial asset – one that, per Ocean Tomo’s research, now makes up the overwhelming majority of corporate market value – gets recognised, defended, and priced correctly at the moments that matter: acquisition, merger, funding, and exit.

The most common failure among UK professional services firms is treating the absence of a balance sheet figure as the absence of value. It isn’t. It’s an accounting rule, not a verdict on worth.

The firms that come out ahead in a transaction are the ones running the two-asset model well before the transaction is on the table – tracking the KPI schedule for their in-house brand equity quarterly, not producing it retrospectively when a buyer asks.

The one thing to do today: if your firm has never had its brand equity formally assessed and does not have a KPI schedule to track it, that’s the gap to close before you negotiate from a position where someone else holds the only number in the room.

A free brand audit is the structured starting point – it identifies exactly where your brand is losing commercial ground, and what a defensible valuation position would need to look like before your next growth, acquisition, or repositioning decision.

FAQs

What is the difference between brand valuation and brand equity?

Brand valuation assigns a specific monetary figure to a brand using cost, market, or income-based methods. Brand equity refers to the strategic and psychological value a brand holds for customers, without attaching a monetary figure to it.

Why doesn’t my brand appear as an asset on my balance sheet?

Yes – this is normal under IFRS and UK GAAP. Accounting standards only permit capitalisation of intangible assets, including brands, once their value has been established through an arm’s-length transaction. In-house brand equity is deliberately excluded.

Which brand valuation method should a professional services firm use?

Income-based valuation is generally the strongest choice for an established professional services firm, since it captures the fee premium and client retention the brand actually produces, rather than historical spend or borrowed market comparisons.

How is brand value affected by an acquisition?

Once a brand is acquired, its value is typically capitalised as goodwill or a purchased trademark on the acquirer’s balance sheet, then reviewed periodically for impairment. Kraft Heinz Company’s 2019 write-down shows how quickly that value can be reversed if brand management falters post-acquisition.

Is it true that only large listed companies need brand valuations?

No – private mid-sized firms preparing for a sale, merger, funding round, or partner buy-in face the same valuation question, typically with less internal financial infrastructure to answer it credibly.

What is purchase price allocation, and how does it relate to brand value?

Purchase price allocation is the accounting process of assigning a portion of an acquisition’s purchase price to specific identifiable assets, including brand intangibles, immediately after a deal completes. It determines how much of the deal value is attributed to the brand itself.

How often should brand equity KPIs be reviewed?

Quarterly review is the practical minimum for a firm preparing for a future transaction, since it builds a multi-year evidence trail of client retention, price premium, and pitch performance rather than a single point-in-time estimate.

Can a strong brand increase what a buyer is willing to pay for a firm?

Yes – a documented price premium, above-average client retention, and strong reputation-driven pitch win rates give a seller’s advisers concrete evidence to defend a higher valuation during negotiation, rather than relying on the buyer’s own assessment.

What is the relief-from-royalty method?

The relief-from-royalty method estimates brand value by assuming a company would pay a royalty to license its own brand name from a third party if it did not already own it, and then capitalising that saved royalty stream.

Is brand valuation the same across every professional services sector?

No – it depends on transaction frequency and comparability within the sector. Law and accountancy have more frequent, better-documented mergers than niche advisory sectors, making market-based comparisons more reliable in those fields than in less-traded specialisms.

What causes a brand impairment after an acquisition?

A brand impairment occurs when a previously capitalised brand’s value is formally reassessed downward, typically triggered by underperformance against the original acquisition case, changed market conditions, or – as in Kraft Heinz Company’s case – brand-damaging operational decisions made post-acquisition.

Should a rebrand happen before or after a valuation exercise?

A valuation exercise before a rebrand establishes a documented baseline, making it possible to demonstrate the commercial impact of the rebrand itself when the next valuation event – sale, funding, or partner buy-in – arrives.